Withnail and I’s drug dealer Danny knew exactly when the 1960s were over. “They’re selling hippie wigs in Woolworths, man. The greatest decade in the history of mankind is over,” he lamented in the cult classic.

On Tuesday, Coinbase hailed the “secular tailwind of crypto adoption among institutions”. But in a week of malfunctioning stablecoins, unexpected bankruptcy chatter and widespread carnage, might that statement alone signal that the glory days for digital assets have well and truly passed?

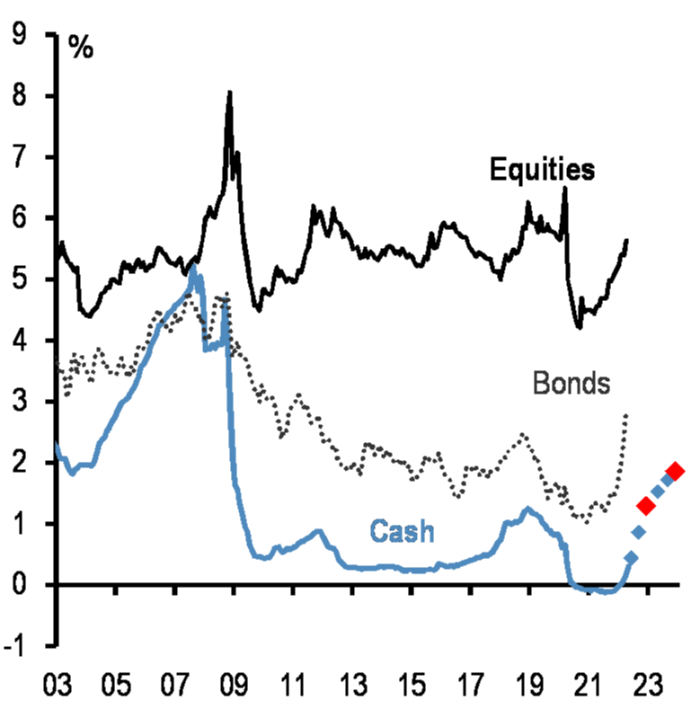

From Morgan Stanley:

Chainanalysis very roughly estimates that institutional investors (anyone with more than $10mn to play with) accounted for 44 per cent of total crypto trading at the end of the second quarter of 2021, up from 8 per cent less than a year before.

Analysts at data provider VandaTrack point out that much of that interest centres on Bitcoin and Ethereum:

Bitcoin was meant to serve as a hedge against inflation, untethered from central bank policy. Alas, its seepage into the mainstream means it now behaves just like any other risky asset.

Interestingly, Morgan Stanley reckons that crypto is more sensitive to the money supply than changing interest rates. “Crypto prices rose in 2020 and 2021 due to central banks increasing fiat money supply,” the bank notes. “Now the Fed is tightening, crypto and equity markets are correcting lower.”

The section in bold implies that cryptocurrencies – and equities – might have further to fall once the Fed starts trimming its $9tn bond portfolio in June.

Analysts at JPMorgan estimated last week that bond yields have a further 200 basis points to rise before the equity risk premium declines to pre-Lehman crisis norms.

Bitcoin may be up at pixel time, but that doesn’t mean a floor has been established. Camberwell carrot, anyone?