Meyrick Chapman is the principal of Hedge Analytics and a former portfolio manager at Elliott Management and bond strategist at UBS.

It would have been fun to eavesdrop on the European Central Bank’s meeting in April. The eurozone monetary family shindig was probably even more tense than normal.

On one side of the room are the inflation-allergic Germans and their (relatively) newfound friends. On the other side those freaking out about the damage higher rates will do to their economies and debt burden.

In the end, last month’s press conference suggested the hard-nosed family members won the day. It seems the ECB will soon follow the Federal Reserve and raise interest rates. Christine Lagarde basically said as much last week. The ECB may even start to reduce their holdings of government debt at some point.

There was probably some grumbling from some family members. The grumbling has probably increased since.

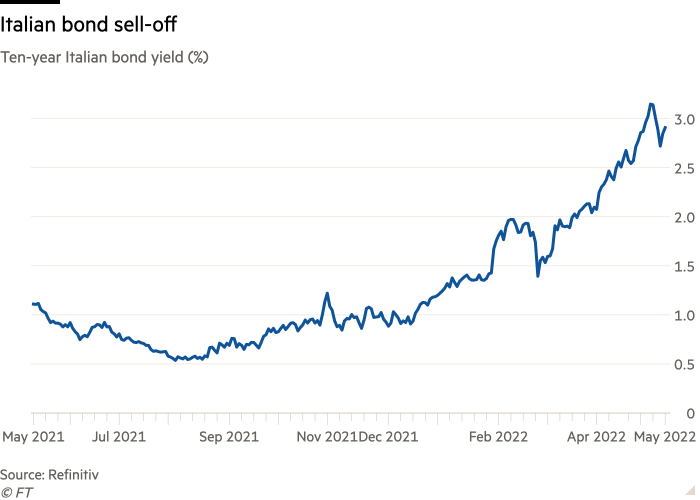

Yields on Italian debt have shot higher and spread to German 10-year bonds has widened a lot. There have been references in bond markets to president Lagarde’s famous quip from March 2020 that the ECB is “not here to close spreads”.

Social media is awash with commentators metaphorically rubbing their hands at the prospect of another European sovereign problem emerging just as the ECB’s asset purchase programmes are winding down.

But isn’t the lesson of the dysfunctional eurozone family that they always seem to threaten a fight on the front lawn, then end up grudgingly hugging and going back inside together? There’s at least a chance that will be the outcome again this time.

No one is pretending that European rates are going as high as those in the US. The entire ECB policy shift seems as much an effort to stop a steep decline in the euro as it is an attempt to rein in inflation. And while rates may rise and the ECB asset purchases may end, there are a few tricks that can be deployed if things get unruly.

There’s the ECB’s hotly anticipated ‘crisis management tool’, which is reportedly in the works. So far, the details are a well-guarded secret. Maybe it will resemble something like the OMT scheme — though hopefully without the shame.

It is equally possible the tool will rejig existing asset portfolio. The Pandemic Emergency Purchase Programme (PEPP) has purchased nearly €1.7tn of government bonds. Unlike the earlier Asset Purchase Programme (APP), the PEPP guidelines are remarkably flexible.

Here are some snippets from the statement announcing it, with FTAV’s emphasis:

And from a subsequent statement:

Reinvested securities surely will follow the same permissive allocation as the original PEPP investments.

So, it’s possible the ECB may raise interest rates and start QT to unwind asset purchases in some member states (like Germany) while its reinvestment programme continues to buy additional securities of vulnerable member states.

It is not often you see a central bank simultaneously ease and tighten policy. Such flexibility has become a hallmark of an ECB that has needed to be creative to keep the family together.

You can be sure that if a pandemic can be used to introduce such flexible rules, a European war will present an ideal excuse for creativity. As the Council said when they announced the PEPP in March 2020:

Moreover, if that all fails and peripheral yields continue to rise, there is always the prospect that domestic investors will ride to the rescue.

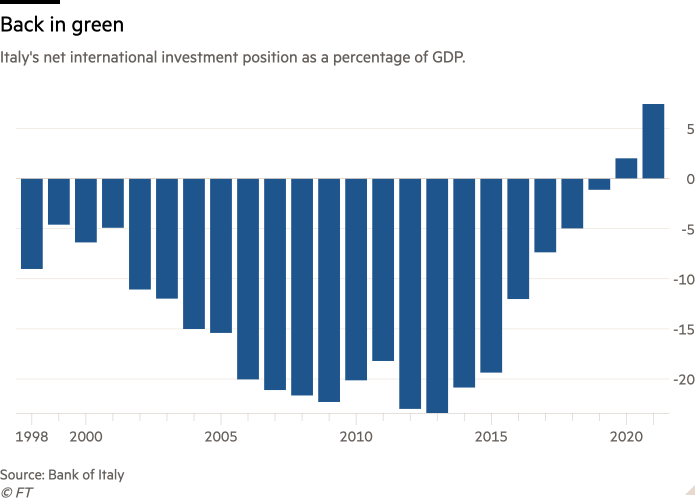

When Italian 10-year government yields rose above 4 per cent in 2011, Italian investors enthusiastically bought their own debt even as foreigners sold on concerns about Italian fiscal sustainability. When Italian yields fell below 4 per cent in 2014, the domestic buying stopped, and Italian investors started to buy foreign assets for higher returns.

Notably, Italy’s net international investment position has swung from a big deficit to a big surplus. With Italian yields rising to over 3 per cent earlier this month, and financial markets everywhere looking risky, it may not be long before domestic investors start to buy Italian bonds again, irrespective of ECB policy.

They may be gratified to know that the substantial PEPP reinvestment programme may be persuaded to over-allocate to Italian government bonds if things continue to be challenging.