Good morning. Who cares if Elon Musk buys Twitter, the whole thing is stupid and annoying, let’s all do our best to ignore it. So it’s the US economy, and more on Russian oil, below.

Also, we’re taking Monday off. While we’re away, try other good FT Newsletters, like Moral Money (sign up here) and Working It (here). Email us: robert.armstrong@ft.com and ethan.wu@ft.com.

A little less demand would be really good right about now

If the measure of economic strength is low unemployment, the US economy has been growing leaps and bounds. Yes, recession talk is everywhere, but not because of any obvious sign of stagnation, but rather because the labour market is so strong that a Federal Reserve-induced recession may be the only thing that could bring inflation under control.

But there are signs that the economy is slowing, even though policy tightening has barely begun. This might be good news. If growth slows on its own — if, specifically, demand slows on its own — the Fed might not have to resort to shock tactics. The very worst outcomes, such as a deep recession or a meltdown in housing or stock markets, might just be avoided.

There is no question that growth is slowing globally. As our friend Edward Al-Hussainy of Columbia Threadneedle pointed out in a recent note to clients, in recent weeks German economists are slashing their outlook for the country’s growth, because of the impact of the war; the World Trade Organization has cut global trade forecasts due to war and Covid; and the IMF is cutting its outlook too. But a lot of this is about supply restrictions curtailing growth, which is unlikely to help with inflation. What is needed is cooler demand:

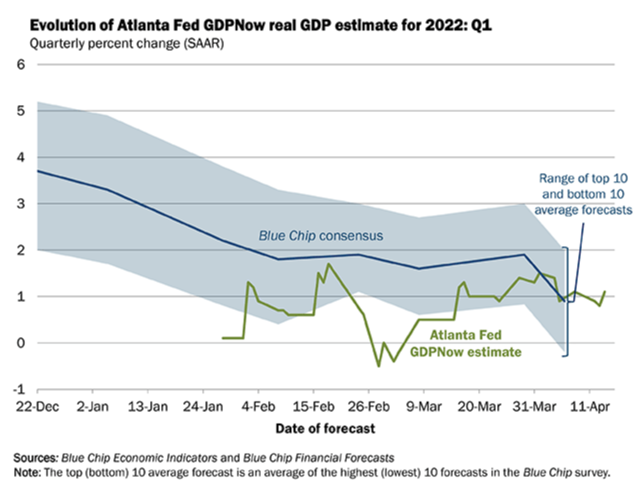

In this context, note that as low as unemployment is, US real gross domestic product growth is hardly screaming. Here is the Atlanta Fed’s first-quarter estimate:

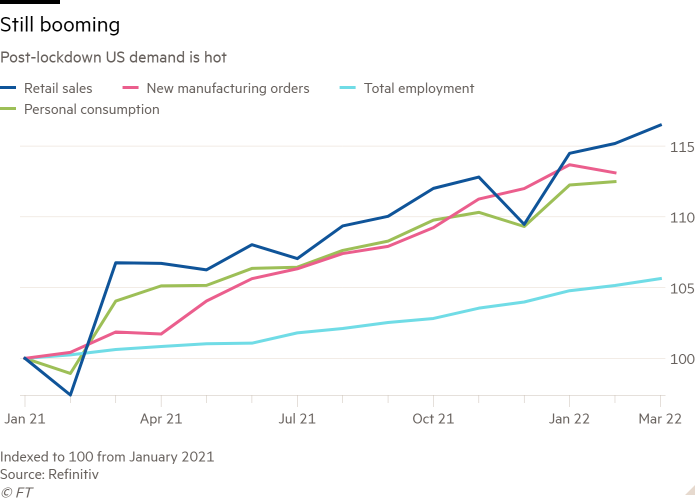

And some of the softness in that chart may reflect moderating demand. After years in which cooped-up consumers spent their stimulus cheques ordering air-fryers on Amazon, it was a relief to see quite a soft retail sales report for March. The headline figure, a 0.5 per cent increase from February, was distorted by a huge 9 per cent surge in petrol station sales. Strip those out, and retail sales fell 0.3 per cent. And once you account for inflation, the picture looks still weaker, as Andrew Hunter of Capital Economics notes:

The retail report matches up with February’s 0.4 per cent decrease in real personal consumption spending.

The obvious place to look for lower demand is housing, where anticipation of Fed tightening has been sufficient to push mortgage rates to 5 per cent. Because US housing supply is extraordinarily tight, it is not perfectly clear how much higher ownership costs will affect sales volumes, and therefore all the activity, from furniture-buying to renovation, associated with home purchases. But there will be some effect.

Beyond that, there is something of a grab-bag of data and anecdata that suggest softer demand. We’ve already written about US trucking and shipping rates falling. Shipping across the Pacific is getting cheaper too, and that might not all be down to lockdowns in China.

The US doesn’t necessarily need contracting demand. In areas like investment that could do productivity damage in the long run. Growth that is gentle enough to give stressed supply a break would be just the thing. A calm little slowdown may be our best shot at avoiding a nasty big one. (Armstrong & Wu)

No, Russia cannot just send its oil to China

It is often argued that if Europe and the US won’t buy Russian oil, someone else will, and that therefore sanctioning Russian energy exports would be futile. China is the replacement buyer most often mentioned.

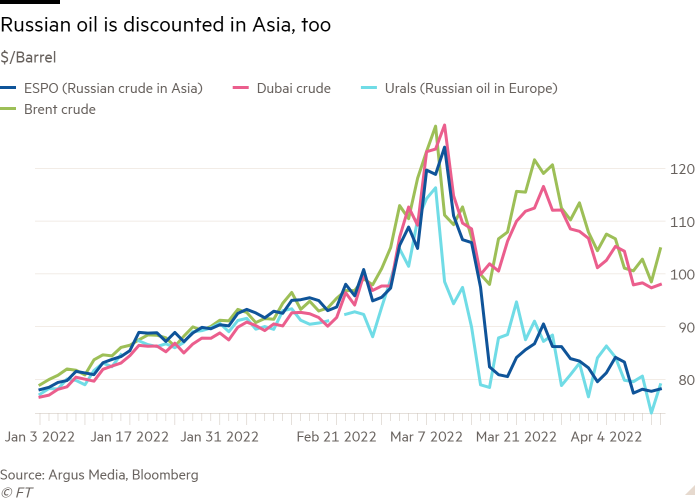

This is probably wrong. A few days ago, we ran this chart:

The light blue and green lines show you that since the invasion of Ukraine, Russian Urals crude piped out in the Baltics or the Black Sea sells at a huge — 20-25 per cent — discount to benchmark Brent in Europe. The dark blue and pink lines show something more interesting. Russian oil piped from Taishet in eastern Siberia to Kozmino on the Sea of Japan sells at a big discount to the local alternatives. The biggest buyer of this Eastern Siberia Pacific Ocean crude is Chinese refineries.

We know the discount has nothing to do with low Chinese demand due to Covid, because China is not buying crude from the Middle East and Africa at similar discounts. We also know that Chinese Espo imports have not increased noticeably. What is going on? One analyst I spoke to argued that the threat of future sanctions is having an effect:

Furthermore, it seems unlikely that Russia will be able engineer a long-term change in buying patterns, such that China buys Russian output, and output from the Middle East and Africa shifts toward Europe. Here is Bill Farren-Price, a director at the energy consultancy Enverus:

China cannot solve Russia’s oil export problem.

One good read

A great cover piece in this weekend’s FT Magazine, on the succession crisis facing Japanese small businesses.