Manmohan Singh is a senior economist at the IMF. The views below are his own, rather than that of the IMF or its executive board.

Every year around April I go through the annual reports of the big banks. It’s a fascinating exercise. But the real gold nuggets are often found in the footnotes, which most analysts never read.

The latest numbers indicate that “collateral velocity” — a measure of how quickly and smoothly collateral moves around the financial system — has started slowing again.

That indicates a need to augment the current financial plumbing, and raises a few issues that warrant attention from policymakers.

First, some background. Collateral velocity is simply the ratio of the total pledged collateral received by the large banks, divided by the primary collateral sourced from reverse repos, securities borrowing, prime brokerage and derivative margin. This ratio measures the reuse of collateral due to financial intermediation between banks and non-banks, also known as “collateral chains”.

For global banks that are active in peddling pledged collateral globally, there are two primary sources of collateral that form the basis of the bank/non-bank nexus, and the market plumbing: hedge funds and other types of institutional investors.

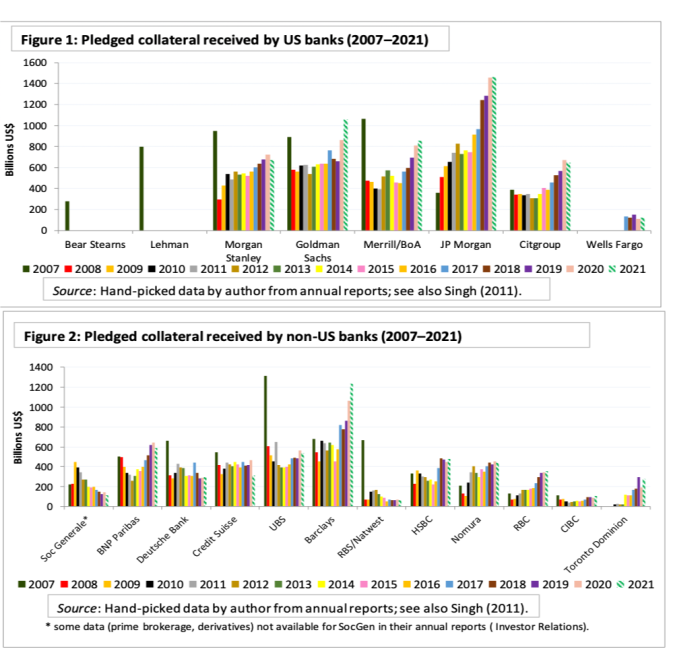

For example, in 2007 about $3.4tn of “source collateral” was provided by hedge funds (via their repo and prime brokerage funding), securities lending by pension funds and insurers, and via derivative margins. Given the overall pledged collateral of $10tn, this meant an overall collateral velocity (or reuse rate) of about 3.

The original estimates of collateral velocity were first calculated in 2011. Researchers from Bank of England, Dutch Central Bank, Reserve Bank of Australia, and recently Bundesbank, and public-and-private regulators, (FSB and DTCC etc) have since been investigating this topic, including several working groups at BIS.

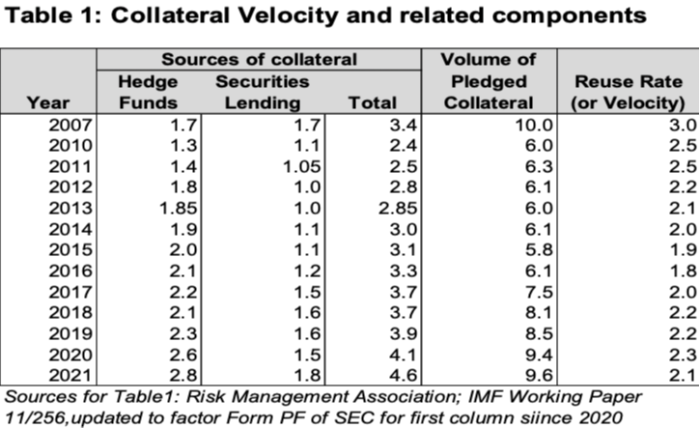

As you might expect, a lot has changed since 2007, with the disappearance of Lehman Brothers and Bear Stearns, the reshuffling of business models by UBS, Credit Suisse and Deutsche Bank, and the rise of JPMorgan and Barclays. The latest data is in green-and-white bars below.

Although dealers adapted to the post-Basel regulatory era and balance-sheet space constraints, re-use capacity has maxed out in recent years. Despite an increase in the sources of overall pledged collateral, balance sheet constraints limit only reuse in markets that are more profitable — for example, prime brokerage transactions are preferred over repo.

Changes in hedge fund strategies have been the primary drivers of the altered landscape, as banks have worked to accommodate their customers’ preferences. The size of the hedge fund industry has grown above $4tn of assets under management, but it is important to understand their footprint (leverage) and their choice of funding.

In the period 2019/20 we saw a shift from equity strategies (in prime brokerage) to fixed income strategies (in repo); then a reversal towards prime brokerage after the March 2020 crisis. Leverage also reshuffles with such strategies (repo is higher leverage than equity strategies).

The initial post-2008 slump in collateral velocity was caused by a spike in counterparty risk aversion between large banks in the aftermath of Lehman Brothers’s demise. But it has remained subdued ever since, despite increasing sources of collateral in recent years.

Factors like the European crisis, quantitative easing (central bank bond purchases restricted the availability of good collateral) and regulations that now restricted dealer banks’ intermediation capacity have had a big impact. After ticking up a little from the post-crisis doldrums, the collateral velocity fell back to 2.1 last year.

Dealer balance sheet constraints and the collateral reuse metric are a harbinger for market plumbing issues. For example, the debt pipeline is likely to be sizeable relative to dealer balance sheet capacity to arrange transactions in all collateral markets (like repos/sec-lending/prime brokerage/derivatives). This is especially true in the US.

If balance sheets are constrained, prime brokerage and derivatives transactions are generally more profitable per unit of balance sheet, although banks continue to seek creative netting solutions (like FICC) to make repo attractive.

But the interest rate cycle is turning. Collateral constraints in some jurisdiction (such as the eurozone) mean we will need to revisit dealer balance sheet constraints, as repo markets will need to move in tandem with rate hikes. Basically, the “old pipes” are maxed out, so new pipes are needed to augment the traditional ones, and bring the global financial plumbing into the new century.

As a result, there are a few issues that warrant attention on the policy front:

• If new pipes are not forthcoming, we may need regulatory or central bank intervention to prevent unavoidable systemic risk. But in the the aftermath of the financial crisis and the Covid-19 pandemic, the central bank footprint in market is already large.

• Inter-operability, including tri-party links, is crucial to mobilise collateral. Global custodians such as Euroclear, Bank of New York or Clearstream — often called “International Central Securities Depositories” — are trying to enhance links with country-specific CSDs, but local laws often hinder such ties.

• Tokenisation maybe a silver lining on the horizon. Frictionless collateral with instant, realtime settlement can increase the velocity of collateral, if the new technology can work within the regulatory parameters.