LG’s battery business delivered South Korea’s biggest-ever initial public offering last week, helped by frenzied interest from millions of ordinary Koreans convinced that US-China tensions will drive global carmakers to its technology.

“It is the biggest news in the stock market. I really don’t want to miss out on an opportunity like this,” said Bae Sung-hoon, an office worker who subscribed to LG Energy Solution’s IPO. “The shares will go up, as electric vehicle batteries are one of the country’s most promising industries.”

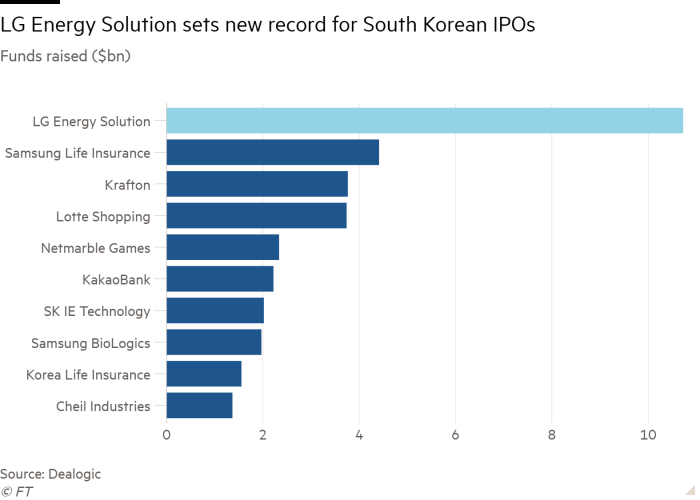

The $10.8bn share sale gives the company a roughly $70bn valuation, behind only Samsung and SK Hynix in South Korea. A record 4.4m retail investors placed Won114tn ($96bn) in bids, ultimately taking home a quarter of shares sold.

But the listing is only a prelude to the real battle ahead as LGES seeks to challenge the dominance of China’s $200bn battery giant Contemporary Amperex Technology — an ambition bankers and industry experts say the Korean group might just achieve.

“LGES is already leading the industry in terms of technology, although it is lagging behind CATL in volume,” said one investment banker close to the deal. “The IPO success shows that investors are positive about LGES’s growth prospects as the funding lends credibility to its growth plans.”

James Lim, an analyst at California-based hedge fund Dalton Investments, is among those who see the company benefiting from “the intensifying technology war” between the US and China, which he believes will give non-Chinese battery producers an advantage among American and European customers.

“This will help LGES increase its global market share while CATL may find it more difficult to expand abroad,” he said.

Yet challenges remain before South Korea’s battery champion can close the gap, and some investors question whether the company can overcome quality issues to beat the competition on market share and profitability.

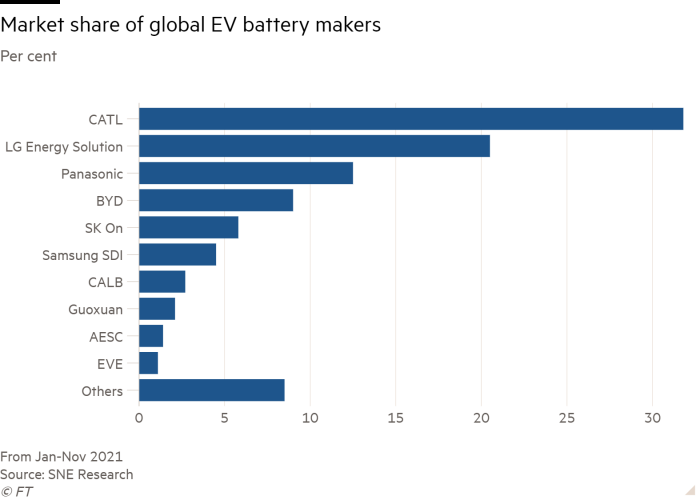

Electric vehicle sales are forecast by Deloitte to increase more than 12-fold this decade to 31.1m a year, accounting for almost a third of all new vehicles by 2030. LGES controls about 20 per cent of the global EV battery market against CATL’s 32 per cent, according to figures from SNE Research.

LGES ranks among the industry’s worst performers on profitability, posting losses in both 2019 and 2020. Last year it reported an operating margin of 5.9 per cent, less than half of CATL’s estimated 12.5 per cent, according to SK Securities.

“CATL is a very profitable company thanks to its cost advantages,” said Lee Chai-won, chair of Life Asset Management, referring to China’s cheaper labour costs, easier access to raw materials and generous state subsidies for local battery producers. “Despite LGES’s funding advantages, it won’t be easy to boost profitability amid intensifying competition.”

What LGES does have is the backing of the wider LG Group, one of South Korea’s biggest conglomerates, which owns the battery producer through its subsidiary LG Chem. LGES, which has offshore plants in Poland, the US and China, plans to invest about Won8.85tn in those plants by 2025, with an aim to almost triple capacity.

“The IPO is absolutely critical in driving the growth and will give the competitive edge to scale up relative to others,” said Neil Beveridge, an analyst at Bernstein.

LGES, which has joint ventures with General Motors, Stellantis and Hyundai Motor, is now focused on expanding in the US. SK Securities forecasts that by 2025, almost half of all electric vehicles made in the US could use the company’s batteries.

With Chinese subsidy rules favouring domestic companies, Beijing’s industrial policy is also pushing South Korean companies to diversify away from the world’s largest EV market.

“CATL is heavily focused on China and struggling to go global while LGES is doing well in global markets outside of China,” said Choi Joon-chul, head of VIP Research and Management.

And while China produces 70 per cent of global lithium-ion batteries, Beijing is ending subsidies for Chinese producers next year and analysts expect CATL’s margins to come under pressure.

“In the long run, given the decoupling, we are seeing [between China and the west] . . . it creates opportunities for companies outside of China, in particular LGES, which is the biggest-scale competitor to CATL,” said Beveridge.

Kwon Young-soo, LGES’s new chief executive, has predicted its share of the global market will eventually eclipse CATL’s. But serious flaws in some of his company’s batteries, which forced GM and Hyundai to conduct some of the industry’s most expensive recalls, have spooked some investors. And other key customers including Tesla and VW plan to internalise their battery production.

“Resolving the safety problems is very important for its partners like GM”, said Lim. “The company will be pushed out by rivals if it can’t.”

Rising input prices are also adding urgency to the LGES drive to reduce its dependence on rare earth elements in China, where rocketing EV sales have led to shortages in the metals vital to battery production.

LG Chem is set to invest $5.2bn in the production of EV battery chemicals and materials by 2025. But Yoon Hyuk-jin, an analyst at SK Securities, said the group still “needs to invest more in upstream projects to boost its supply chain stability”.

In the near term, investors are focused on how the battery maker’s shares fare when trading begins on Thursday.

“The stock price will easily double the IPO price, given all the fanfare about EV batteries. Then, I will just cash out,” said Shin Geum-ok, a housewife, who received 19 shares after placing bids worth Won360m.

But after companies raised a record Won17tn on Seoul’s Kospi market last year, some fear a poor showing from LGES could dent appetite for big listings that are in the pipeline, including Hyundai Engineering, Kakao Entertainment and food delivery platform Market Kurly.

Other South Korean groups may have trouble replicating LGES’s spin-off success, VIP’s Choi warned, noting that regulators were increasingly focused on shareholder complaints against companies hiving off businesses for listings that dilute existing shareholders.

“It won’t be easy for Korean companies to pursue these kinds of splitting and listing tactics.”